Your Car Is Parked 23 Hours a Day

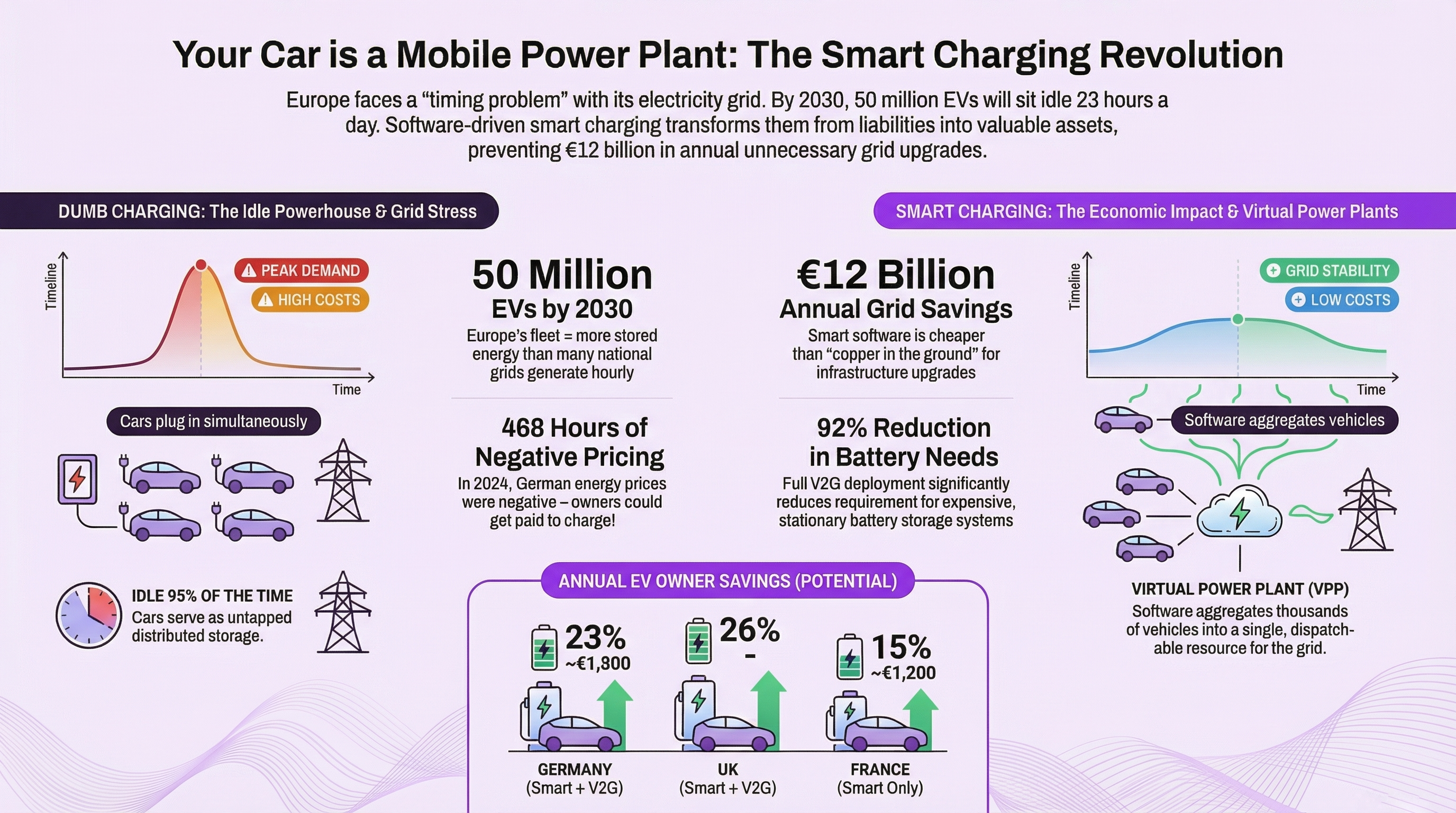

By 2030, 50 million electric vehicles will sit on European driveways. If they charge dumb, €12 billion a year in unnecessary grid upgrades lands on electricity bills. If they charge smart, some owners will be paid to plug in. Europe's electricity grid does not have a generation problem. It has a timing problem.

Europe is building the most sophisticated distributed energy storage system in history, yet it is unaware of this fact. By 2030, more than 50 million EVs, each with a capacity of between 40 kWh and 100 kWh, will be on the continent's roads. Collectively, they will represent more stored energy than many national grids can generate in an hour. The engineers who designed these vehicles built the hardware for a revolution. However, the software that would make that revolution useful mostly doesn't exist yet.

On a windy Tuesday night in northern Germany, wind turbines push more power into the system than anyone needs. Prices go negative, which means that energy suppliers literally pay someone to take the electricity. In 2024, Germany recorded 468 hours of negative electricity pricing, up 60% year-on-year. Meanwhile, roughly 9.3 million battery electric vehicles sat parked across European roads, most of them plugged in at peak evening hours, drawing expensive power at exactly the wrong moment.

Europe has built a growing fleet of mobile batteries (each carrying between 40 kWh and 100 kWh of storage capacity) and almost none of them are doing anything useful for the grid. They charge when energy is priciest, sit idle when it's cheapest, and return nothing. The technology to change this exists. The economics are compelling. The regulatory framework is catching up. What's missing, largely, is the software connecting all three.

The 23-Hour Battery

Cars sit idle roughly 95% of the time. The average European driver covers around 35 kilometres per day, which means the typical EV uses its battery for about one hour out of every twenty-four. For the remaining twenty-three hours, that battery, representing a significant share of household capital, sits in a parking space doing nothing.

Aggregate that across Europe's current fleet and the numbers become hard to ignore. A study by EY and Eurelectric published in March 2025 projects more than 50 million EVs on European roads by 2030. If that fleet shifted its charging to optimal hours (absorbing surplus wind and solar instead of competing with evening demand peaks) European grid operators could save a projected €4 billion per year in avoided network investment costs.

In a report published in for Transport & Environment calculated that the EU's energy system could save €22 billion annually by 2040 with the full deployment of vehicle-to-grid (V2G) technology, for a total savings of more than €100 billion between 2030 and 2040. Additionally, it would reduce the need for stationary battery storage by up to 92%. These are not advocacy numbers. These are engineering numbers.

What Demand-Side Flexibility Actually Means

Demand-side flexibility (DSF) means consumers (households, businesses, fleet operators) adjust when they consume electricity in response to price signals or grid conditions. The grid doesn't need you to use less energy. It needs you to use it at different times.

For EV owners, the mechanism is straightforward. Instead of charging at 6 PM when half of Europe plugs in simultaneously, a smart charging system waits until 1 AM, when wind generation is high and demand is low. You wake up to a full battery. The grid avoided a stress event. And depending on your energy contract, you paid a fraction of the peak rate.

The Ember Energy think-tank, tracking European DSF markets across 30 countries in their November 2025 analysis, noted that the EU agreed enabling rules for demand flexibility back in 2019, but national implementation has been slow and uneven. The European Commission plans to approve a new Network Code for Demand Response in early 2026. Member states will be required to set national flexibility objectives by January 2027.

The Numbers in Your Driveway

Let's put actual figures on the savings opportunity, because the abstractions hide a concrete reality.

The EY/Eurelectric study modelled total cost of vehicle ownership across six European markets. In Germany, a family car EV owner who charges optimally and participates in V2G services could reduce annual ownership costs by 23%, roughly €1,800 per year. In the UK, SUV owners could see savings up to 26% annually. In France, smart charging alone (without V2G) could reduce a family car owner's total costs by 15%, or €1,200 annually.

In the Netherlands, Dutch motoring association ANWB ran a smart charging pilot through 2023–2024, connecting EV owners directly to the European Power Exchange (EPEX SPOT). Drivers plugged in and let the algorithm optimise charging around live energy prices. During one 12-hour session on 1 May 2024, when negative energy rates were in effect, a Tesla Model Y driver received a payout of €7.62, paid to charge the car. That's not a marketing stunt. That's what a functioning flexibility market looks like when it reaches an ordinary household.

"Most EV owners are sitting on this option right now and don't even know it. The technology exists. The market is forming. Regulatory frameworks are catching up." Peter Hofierka, co-founder of Wattiva

The Aggregation Equation

Individual EVs don't move markets. But aggregated EVs can.

When thousands of vehicles are coordinated through a single software platform, their combined battery capacity becomes a dispatch-able resource called Virtual Power Plant (VPP). The platform reads grid signals, energy prices, and each vehicle's individual charging schedule, then optimises across the entire fleet in real time. No single driver does anything differently. They plug in, set a departure time, and the software handles the rest.

The scale implications are significant. By the end of 2024, it is estimated that there will be 7.5 million private charging points across the EU. More than nine in ten EV charging sessions will happen in private settings, such as homes, workplaces, and depots. These 7.5 million charging points represent a significant amount of potential flexibility that remains largely unused as grid assets.

Some forecasts project demand-side flexibility capacity in Europe to grow at a compound annual rate of 9% through 2050. However, it is noted that as of 2025, the market remained significantly underutilised, with barriers including low smart meter adoption (fewer than 20% of German households had them in early 2025) and regulatory frameworks that still prevented independent aggregation in several major markets.

The Regulatory Inconvenience

Here is where the honest version of this story gets complicated.

Europe's demand flexibility ambitions are genuine, but the architecture is fragmented. France has a relatively mature flexibility market, though upcoming capacity market reforms in 2026 are expected to reduce revenue for aggregators. Germany has high wholesale price volatility (theoretically ideal for smart charging) but independent aggregation is currently prohibited, meaning DSF providers must operate through electricity suppliers rather than accessing markets directly. Poland has emerged as an exception, implementing an independent aggregator framework that allows flexibility providers to participate across multiple markets. The Nordics, Spain, and Britain remain among the best-performing implicit DSF markets in Europe.

The European Commission's forthcoming Network Code for Demand Response should reduce some of this fragmentation. Whether it resolves the interoperability gap between EV manufacturers, charger hardware, and energy management software is a separate question, and a harder one. Studies flagged the lack of standardised bidirectional charging protocols as the primary technical bottleneck holding back V2G deployment at scale. The ISO 15118-20 standard exists. Mandatory adoption across all new EVs does not yet.

Building the Infrastructure That Already Exists

The most pointed argument for smart charging is architectural, not financial. Europe does not need to build grid infrastructure in proportion to EV adoption if it can use the distributed storage it already has.

Eurelectric's Grids for Speed study estimated that demand-side flexibility, led by EVs, could reduce annual European grid investment requirements from €67 billion to €55 billion between 2025 and 2050. That €12 billion annual gap represents cables, substations, and transformer upgrades that don't need to happen if the cars on European driveways are managed intelligently. To put it plainly: smart software is cheaper than new copper in the ground.

By 2030, EVs could contribute 4% of Europe's entire annual power supply, enough to power 30 million homes per year, according to the EY/Eurelectric analysis. That number is not contingent on exotic technology. It requires only that the vehicles already being manufactured and sold charge at smarter times.

Wattiva Software as Grid Infrastructure

Wattiva is an energy technology platform built by the team behind Voltia (pioneers in Central European fleet electromobility since 2011). The platform's core proposition is simple: virtual power plant software for energy companies, aggregating EVs, batteries, heat pumps, and solar panels into a single controllable flexibility resource that lets utilities and grid operators treat distributed consumer assets as a coherent, dispatch-able system.

The product operates without requiring users to change energy supplier or install new hardware. The app connects to the vehicle via the manufacturer's cloud interface, monitors real-time electricity prices and grid load, and automatically schedules charging for minimum cost and maximum grid benefit. Wattiva's platform delivers savings of up to 30% on home charging costs, equivalent to thousands of free kilometres annually. The longer-term roadmap points toward zero-cost home charging, achieved through software-driven participation in flexibility markets, not subsidies.

Wattiva is currently running pilots with utility partners and working toward its first aggregation milestone of 30,000 EVs, approximately 15 MW of dispatch-able flexibility, in EU markets. The company is preparing a seed round to scale the model across Europe. That's not a power plant in anyone's backyard. It's a software-managed fleet of family cars.

"Most electric vehicle owners charge their cars immediately after arriving home, which is often the most expensive possible time and the moment when the grid is most stressed. Our platform automates this process and ensures charging happens when electricity prices are most favourable and the grid is under less pressure, often in the middle of the night, when there is a surplus of cheap energy in the system." Martin Gonda, CEO of Wattiva

"It reduces the need to activate expensive backup sources, supports the integration of renewable energy, and above all reduces the need for hundreds of millions in grid infrastructure investment." Peter Hofierka, co-founder of Wattiva

The Inconvenient Baseline

In 2024, one in four cars sold in Europe was electric. By 2030, the continent's EVs will exceed 50 million. If this fleet is not managed properly, Europe will need to build grid infrastructure to serve the worst-case demand curves that smart charging would have prevented. The additional investment required for this unnecessary infrastructure is estimated at €12 billion per year. This cost would be reflected in electricity bills.

The technology to avoid this problem runs on a smartphone. The barrier is not engineering, but rather a combination of regulatory fragmentation, missing interoperability standards, and the fact that most EV owners are unaware that they have an untapped grid asset that is worth real money.

This will change with software. Specifically, it will change when the software is so seamless that drivers don't need to think about it. They just plug in, set a departure time, and let the system decide when the electrons flow.