How Software Became the Most Important Material in the Energy Transition

Electrification demands 50 percent more copper by 2040. The mines can't deliver it in time. A new class of software is racing to close the gap. This might reshape who controls the grid.

The energy transition has a material problem, and it is not the one being discussed. The shortage of solar panels was solved. The cost of wind turbines came down faster than anyone expected. Battery prices fell for a decade and kept falling. The bottleneck, it turns out, is the oldest, least glamorous part of the system: the copper wire that connects everything together. The world does not have enough of it, cannot mine enough of it in time, and — this is the part that matters — may not need to.

Over the past decade, the world has invested trillions of euros in the most visible parts of the energy transition: sleek EVs, massive offshore turbines, fields of solar panels stretching to the horizon. These are the technologies that land on magazine covers and attract venture capital. But while we've been celebrating them, we've been quietly neglecting the system that connects them all: the power grid.

The problem isn't ambition. We're trying to run a 21st-century energy system on infrastructure logic inherited from Thomas Edison's time. We assume that if we generate enough clean electricity, the rest is simply a matter of burying some wires. Dig a trench, lay some copper, move on.

That assumption runs into a physical problem. We are running out of the copper needed to build it all.

The Metal That Makes Electrification Possible

Copper is to the energy transition what oil was to the 20th century: the material without which nothing moves. From the wiring inside an EV motor to the submarine cables under the North Sea, copper carries the electricity that powers modern life. There is no commercially viable substitute for it at scale.

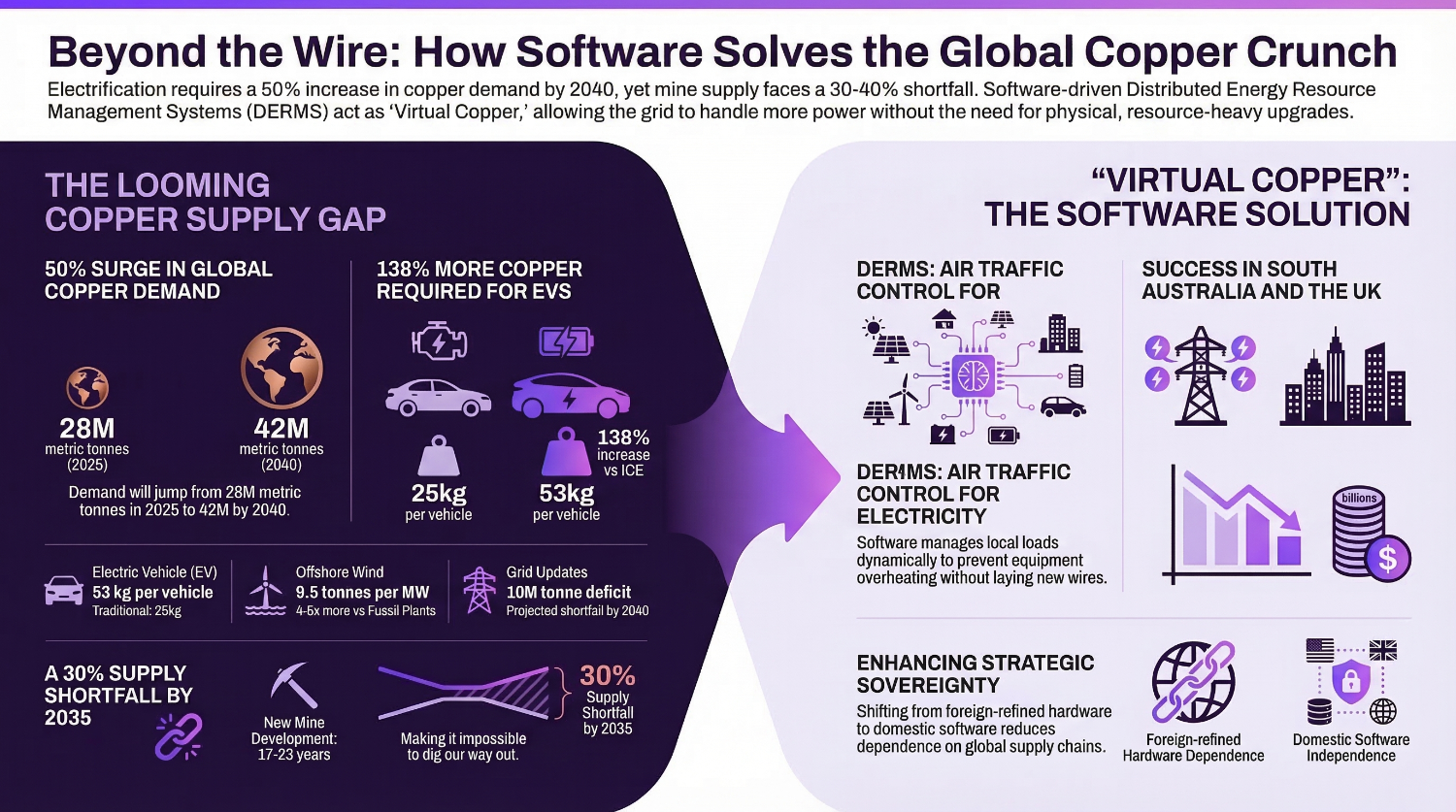

And that's where the trouble starts. Every step toward electrification increases copper demand by multiples, not margins. A typical internal combustion engine vehicle contains roughly 25kg of copper, mostly used in the electrical wiring harness, the alternator windings, and the low-voltage battery. An electric vehicle requires approximately 53 kilograms of copper, representing a 138% increase compared to a conventional vehicle. Some larger EV platforms push that figure considerably higher. An offshore wind turbine uses approximately 9.5 tonnes of copper per megawatt of installed capacity, including its underwater cable to shore, making it four to six times more copper-intensive per megawatt than a conventional fossil fuel plant.

Multiply those ratios across billions of vehicles, millions of turbines, and continent-spanning grid upgrades. S&P Global's January 2026 study projects global copper demand rising from 28 million metric tonnes in 2025 to 42 million metric tonnes by 2040, a 50% increase. The IEA's 2025 Global Critical Minerals Outlook puts it plainly: despite strong copper demand from electrification, the current mine project pipeline points to a potential 30% supply shortfall by 2035, driven by declining ore grades, rising capital costs, limited resource discoveries, and long lead times. Under more aggressive climate scenarios, that gap widens to 35% in the Announced Pledges Scenario and over 40% under a Net Zero Emissions pathway. We want to decarbonize the planet. But we are physically constrained by the material we need to do it.

Why We Can't Dig Our Way Out

For years, the reflexive response to resource constraints has been a shrug. If copper prices rise, the market will respond. New mines will open. Supply will catch up. This reasoning assumes that mining can accelerate as fast as demand grows. It can't.

Mine development timelines now average 17 years from discovery to first production, and only 14 new copper deposits have been discovered in the past decade, compared to 225 in the previous 23 years. In the United States, the permitting and development timeline can stretch to 29 years. We're in 2026. If a significant new mine isn't already well into construction today, it will not contribute meaningfully to supply before the mid-2030s. The mining pipeline for this decade is effectively locked in.

The ore itself is getting poorer. Since 1991, average global copper ore grades have fallen by 40%. Supply is set to peak in the late 2020s at just over 24 million tonnes before dropping below 19 million tonnes by 2035 due to falling ore grades and mine closures. Miners are moving more earth, consuming more water, and burning more energy to produce the same amount of metal. The copper that was cheap and easy to access built the twentieth century. What remains is deeper, lower quality, and harder to reach every year.

S&P Global describes the resulting disconnect as a "systemic risk for global industries, technological advancement and economic growth," projecting a supply deficit of 10 million metric tonnes by 2040 despite an expected more than doubling of recycled copper scrap over the same period.

Replacing Copper with Code

We cannot mine our way to a clean grid fast enough. So the question shifts: what if we could make the grid we already have work harder?

The concept goes by the name demand-side flexibility, though the jargon obscures something quite simple. Instead of laying thicker copper cables every time a neighbourhood adds fifty EV chargers, you use software to manage the load on the cables you already have.

The enabling technology is a Distributed Energy Resource Management System, or DERMS. It functions as air traffic control for your local electricity network. When a transformer starts approaching the point where it could overheat, the system doesn't call for a construction crew. It sends a signal. It might slow down EV charging by a few minutes across a cluster of vehicles. It might draw a small amount of stored energy from home batteries to relieve pressure on a local power line. It might stagger industrial loads by fifteen minutes.

None of these adjustments are noticeable to the person using the electricity. But collectively, they can defer or eliminate the need for physical grid reinforcement — the copper-heavy, multi-year, multi-million-euro kind. In the industry, this is sometimes called "virtual copper": using data to make existing wires behave as if they were thicker. Utilities piloting these systems have found they can extract substantially more capacity from existing infrastructure before any physical upgrade is needed, deferring significant capital expenditure.

This is already happening in markets where the copper ceiling has been hit.

What South Australia and the UK Are Proving

In South Australia, rooftop solar has spread across more than half a million homes, making it one of the most solar-dense grids on the planet. The grid began buckling under its own success. On sunny afternoons with low demand, so much solar energy was being pushed back into the distribution network that voltages spiked, threatening equipment damage and outages. The obvious responses would have been to cap exports, effectively penalizing households for generating too much clean energy, or to spend billions reinforcing substations and feeder lines.

SA Power Networks chose a third option. They developed Flexible Exports: a dynamic system where the grid communicates with household solar inverters every few minutes via the internet, telling each system how much it can export based on the real-time physical state of the local network. When the grid has capacity, households can export up to 10 kilowatts. When it doesn't, the system temporarily dials exports down, sometimes to 1.5 kilowatts. According to SA Power Networks, more than 88% of eligible customers have chosen to opt in. Since July 2023, any new grid-connected solar system installed in South Australia must be compatible with the Flexible Exports standard, and the rollout has now extended to all parts of the state including rural areas on single-wire earth-return networks.

The result: South Australia can accommodate far more rooftop solar on its existing network without the billions in physical upgrades that would otherwise be required. Smart software doing the job that used to require new copper and concrete.

In the United Kingdom, the challenge is different but the logic is the same. The previous first-come, first-served grid connections model led to Great Britain's connections queue growing tenfold in five years, leaving more than 700 gigawatts of generation and storage projects waiting for grid access, around four times what the country needs to deliver clean power by 2030. In December 2025, NESO confirmed a new prioritized pipeline: 132 gigawatts of projects aligned with the UK's Clean Power 2030 target, with a further 151 gigawatts identified as vital to Britain's needs by 2035. According to NESO, the reform is expected to unlock £40 billion in clean investment annually.

Flexibility is not replacing grid investment. It is determining which investments are necessary and when, eliminating tens of billions in reinforcements that would otherwise be built to handle theoretical worst-case peaks that software can manage instead.

The Sovereignty Argument

There is another reason to shift from hardware to software, and it has nothing to do with engineering. It comes down to who controls the transition.

China controls 45% of global copper refining capacity and is projected to increase that share to 50% by 2040. Since 2000, China has accounted for 75% of all growth in global copper smelting and refining capacity. For Europe and North America, an energy transition built purely on physical copper means growing dependence on a supply chain where one disruption in one country can break everything. It means exposure to metals market volatility, to the geopolitics of mining in Chile and the Democratic Republic of Congo, and to refining capacity controlled by a single dominant player.

Software changes this equation. A DERMS platform, a smart grid management algorithm, an optimization model: these are domestic assets. They are built by local engineers, deployed on local infrastructure, and governed by local regulation. When the European Commission identifies hundreds of billions in digital grid upgrades as a priority, the investment stays onshore. The returns stay onshore. The strategic control stays onshore.

This is exactly the kind of problem that Wattiva, a Slovak B2B platform built on deep EV fleet electrification experience, is working on. Wattiva aggregates distributed energy resources such as EV chargers, batteries, flexible loads into dispatch-able virtual power plants. That is giving utilities and energy suppliers the tools to manage grid demand intelligently rather than building around it. The logic is the same whether you're managing a neighbourhood transformer in Bratislava or a regional network in Germany: the cheapest megawatt is the one you never had to build.

Digital grid intelligence doesn't eliminate the need for copper. It reduces how much you need, and how fast you need it. It breaks the bottleneck. And it keeps the decision-making layer of your energy system at home.

What Gets Built From Here

The copper ceiling is real. But it is a constraint, not a verdict.

One path is to keep treating every grid problem as a construction problem: order more cable, dig more trenches, watch costs climb while timelines stretch past our climate deadlines. The other is to accept that in a world where copper supply is structurally constrained, the most urgent challenge isn't generating more clean electricity — it's managing an accelerating demand for copper across EVs, data centers, grid expansion, and renewable generation, all scaling simultaneously while supply is not on track to keep pace.

Physical infrastructure still needs to be built. New transmission lines, upgraded substations, reinforced distribution networks. The IEA, Europe's grid operators association ENTSO-E, and every credible grid analysis confirms this. But digital flexibility determines which of those investments are essential and which only exist because an outdated grid couldn't manage its own traffic.

South Australia's solar owners proved that a five-minute signal to an inverter can do the work of a new substation. The UK's grid reform proved that software-defined connection management can unlock capacity that was supposedly years away from being available. These are not pilot curiosities. They are early evidence of a different theory of infrastructure.

The leaders of the energy transition will not be the countries that own the most copper mines. They will be the ones that build the smartest grids.